Last week, I caught up with my favorite OG volatility fund manager named David Dredge and a few of his colleagues for a coffee. The conversation started off with a discussion regarding how Japan’s financial markets are going gangbusters. The plebes and the corporates there are flush with cash and the spike in inflation is dragging them out of low-to-no yield bank deposits and into the stock and property market.

Then, we turned to the current state of the crypto markets, and Dave asked me: “so what’s going on with the SEC going after Coinbase and Binance?”

I responded that it is just another example of how the fiat financial system is trying to restrict capital from leaving the casino. There is a lot of debt to be repaid, and the system needs as much exit liquidity as possible. He nodded in agreement. Dave likes to refer to the fragile fiat financial system as the Sharpe World. (The name stems from the Sharpe Ratio, which is considered by most risk managers to be a standard measure of how “risky” a portfolio is – when in reality, it’s entirely fugazi, because it looks at probabilistic possibilities rather than the actual outcomes of investment decisions.)

I then added that I believe what happens in the US vis-a-vis crypto is actually quite irrelevant because capital is fungible. (I’ll expand on this thought in a bit.)

Finally, we talked about the impending Chinese yuan (CNY) devaluation. The impetus for this line of conversation was our general disbelief regarding the up and to the right characteristics of Singapore’s current residential property market. Chinese capital does not care how large the tax applied to property purchases is because the yuan is overvalued and the Singapore dollar is undervalued. So even if they must pay a 60% tax to the Singaporean government, Chinese capital sees Singapore property as a cheap bank account with which they can safely store their wealth.

David went on to argue that Beijing will eventually devalue the CNY against the Japanese yen (JPY) because Japan is China’s real global export competitor. The yen has depreciated rapidly against the USD and CNY since the Bank of Japan (BOJ) has continued its money printing activities – called Yield Curve Control (YCC) – while all other major central banks are raising interest rates and reducing their balance sheets. Since COVID, The People’s Bank of China (PBOC) and the Chinese central government have shown relative restraint on the money printing front – which is why the CNY is so “strong” vs. the USD and JPY.

We briefly touched on the fact that Chinese exports have started to falter as the global economy slows. The government will soon need to start creating growth to placate its plebeian comrades, meaning it is about time for the PBOC to adjust its monetary policy and weaken the CNY vs. the JPY and USD. The weaker CNY will help boost Chinese exports at the expense of their Japanese competitors.

As I hopped in my whip to return home, a little thought bubbled to the surface. The current market setup reminded me of the summer of 2015. The nuclear bear market, which started with the implosion of Mt. Gox in early 2014, was quite savage. Volatility and trading volumes collapsed; the sideways price action was excruciating in its boredom. The Bitcoin price hovered around $200 for what seemed like an eternity. But in August of 2015, the PBOC suddenly sparked a rally in China’s interest for Bitcoin with a “shock” devaluation vs. the USD. From August to November of 2015, the price of Bitcoin tripled, with Chinese traders driving the market higher. I believe something similar could happen in 2023.

Since 2021 (when the major Chinese exchanges all ceased operations in Mainland China), Chinese retail’s capital flows into the crypto capital markets have collapsed. The most influential marginal retail buyer shifted from China to the US.

Starting in 2020, the US government (USG) did something unexpected in deciding how to dole out stimulus. Rather than just handing free money to rich people who hold financial assets, the USG distributed money directly to everyone – rich and poor alike. For the mass affluent (a demographic that I will cover in more detail later in this essay, but for now, let’s just call them households that make $100,000 to $200,000 per year), many didn’t actually need government assistance because they didn’t lose their jobs (since they were white collar gigs that could be done at home). They grabbed that free money, headed straight to the financial markets, and had a good ol’ time. Meme stocks, crypto, NFTs etc. were all pumped by US retail investors. As is always the case, a few of these folks made profits large enough to buy Lambos and Richard Mille timepieces, but the vast majority bought the pico top of the market and set themselves up to get REKT as Sir Powell started jacking interest rates in March 2022.

And now that the TradFi Devil is causing trouble for some of Satoshi’s faithful, the market is freaking out regarding the potential removal of the US retail investor from the crypto capital markets. I believe this concern is misplaced, and if you are prompted to sell alongside US-domiciled institutions that feel they have to sell or discontinue crypto services to US persons, you will be just another sucker who bought the top and sold the bottom. Because across the world in Asia, China and Japan’s silent currency war for export competitiveness is going to drive an insane amount of credit issuance by the second largest economy globally. This credit issuance – aka money printing – will ultimately weaken the yuan and prompt some of China’s mass affluent to shift their capital elsewhere. And given the sheer number of individuals that make up the Chinese mass affluent, when they want to “get out”, all manner of hard assets get pushed higher.

I’ll be covering a lot of ground in this essay. I’m going to start by discussing Sharpe World, and why the US will do whatever it takes to keep its subjects believing that their capital is “safest” in the hands of US financial institutions. Then, I will move onto how the fungibility of capital means that even if it is hard or impossible for the mass affluent retail investors of the US to access the crypto capital markets, the wealthy in America will still be able to easily opt out of the fiat financial system and purchase hard crypto assets. This will ultimately lead me – and hopefully, you – to the conclusion that all this consternation over what is going on in the Land of the “Free” is a waste of mental energy. Then, I’ll cover the budding currency war between China and Japan, and how that will move some Chinese capital into crypto through the Hong Kong financial markets. And finally, I will wrap things up with a breakdown of how I am tactically using the indiscriminate selling of shitcoins as entry liquidity into high conviction doggy doo-doo.

David is one of the best and most intelligent derivatives traders I have ever met. I learn something new about the market structure every time we speak. He has spent most of his banking career in the Asia Pacific region. At our last coffee meetup we swapped stories about our favorite bars in Jakarta. He lived there in the late 1980’s, I went often in the 2010’s.

He is quite plugged into the economic establishments of both the East and the West. US Treasury Secretary Janet Yellen was one of his university professors. He sits on various advisory committees for central banks. Every time we meet, he talks about how he tries to get the “adults in the room” to understand that they look at risk in an entirely flawed manner. As I mentioned earlier, he calls it the Sharpe World.

“How do humans manage the risk of death?” Dave asked me rhetorically.

“You don’t do things you know for sure can kill you – even if the per event probability of death is small – and that lengthens your life span.”

I thought about some simple things many humans do to lengthen their lifespan:

If you follow these simple rules religiously, you can eliminate totally avoidable causes of death and (most likely) lengthen your lifespan. What humans don’t do, though, is probabilistically evaluate each of their actions in the moment, determine the likelihood of death, and then take the plunge banking on the odds that they won’t end up on the tails of the distribution. For example, your average bike rider doesn’t look at their helmet and say “that shit is lame – and if I don’t wear it today, it would be a 3-sigma event (<1% chance) if I get in an accident and die. I like those odds.” But they did, and that day ended being a 3-sigma event day, you couldn’t ask God to give you another life because you dutifully used a +/- 2-sigma log-normal probability decision-making rubric and therefore took an appropriate amount of risk … you just dead.

However, in Sharpe World, financial institutions play the odds on the probabilities of death and engage in risky activities all the time. And they do so in large part because they know that, when they die every 5 to 7 years on average, the central banks and governments will be there to bail them out. The system will always bail out the residents of Sharpe World by printing money and debasing the public’s wealth.

Both the government and financial institutions love Sharpe World, because it is a world filled with rules established by super duper smart academics at “elite universities” that tell them exactly what to do and how to act. Everyone follows the rules, so that when things go kaboom, no one can say they were doing anything uncouth. And therefore, it’s not fair for the public to be upset when they must pay up to save yet another highly regulated financial institution that has gone belly up, a la Credit Suisse.

The whole point of this monetary confidence game – all buttressed by unproven economic theories masquerading as laws of nature – is to keep investors buying and holding long-term government bonds. If I, as a government, can convince my subjects to delay consumption and invest their savings with me on a long-term basis, then I am a successful, credible state actor. If, on the other hand, investors would rather only lend to the government on a short-term basis (if at all), then the state is not credible and must resort to unpopular measures (such as high taxes) to pay for goodies.

The indoctrination of the world’s premier financiers into Sharpe World starts early. If you have taken any university level-finance courses, then you have been drilled on the efficient frontier and how there are certain magical assets called government bonds that both increase returns and decrease the overall volatility of a portfolio. Therefore, all a portfolio manager must do is add leverage to long-term government bonds, and voila – their returns go Pump Up The Jam!

As US and developed market bond yields went on a 40-year bull market run, everyone believed they were geniuses. People like Ray Dalio became billionaires many times over by just going long bonds. Every time the market wobbled, they would just apply more leverage, knowing the authorities would print money to squash any sort of real price discovery. Dalio called this the Fair Weather Fund.

But now, following the fastest rise in inflation and short- term rates in many decades, there doesn’t seem to be any reason for investors to hold long-term government bonds. And you readers are all part of this story. Your retirement plan is managed by a public or private pension fund filled with Sharpe World denizens. The fund managers are required by law to invest a large part of your savings into long-term government bonds, because … well, because the government said so. These are the same government bonds that will get eviscerated as inflation rises, but the financial institutions in Sharpe World dutifully follow regulations and lead the capital of their clients to the slaughterhouse because dems da rules! At no point is anyone in Sharpe World buying long-term government bonds with their own money.

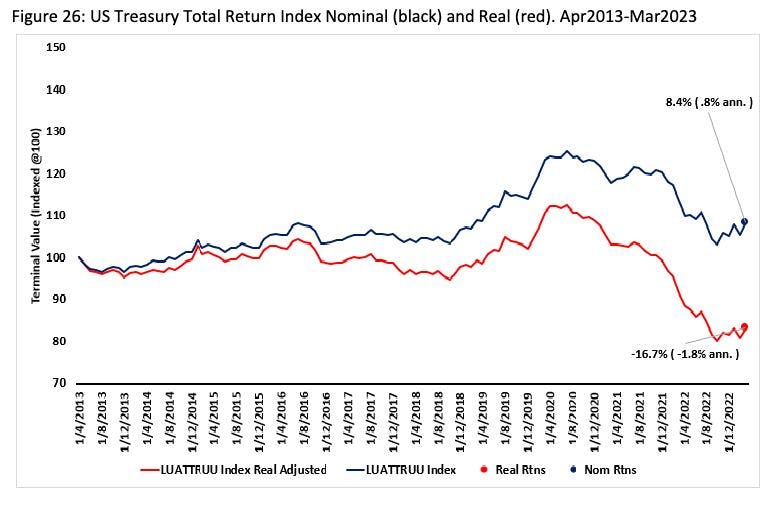

Dave bangs on about this in every one of his monthly letters. His point – which he illustrates with the data that I’ve provided below – is that investors should abandon owning government bonds for volatility reduction and return enhancement because at low rates, these instruments can no longer work their magic. Instead, investors should hold equities, gold, crypto, and long volatility tail hedges.

“Participate and protect,” he says. “My fund provides the protection by owning positively convex derivatives, and you the investor should just buy a basket of equities to participate in the upside.”

This chart clearly shows that over the last decade, owning a basket of US Treasurys (UST) has lost money in both nominal and real terms.

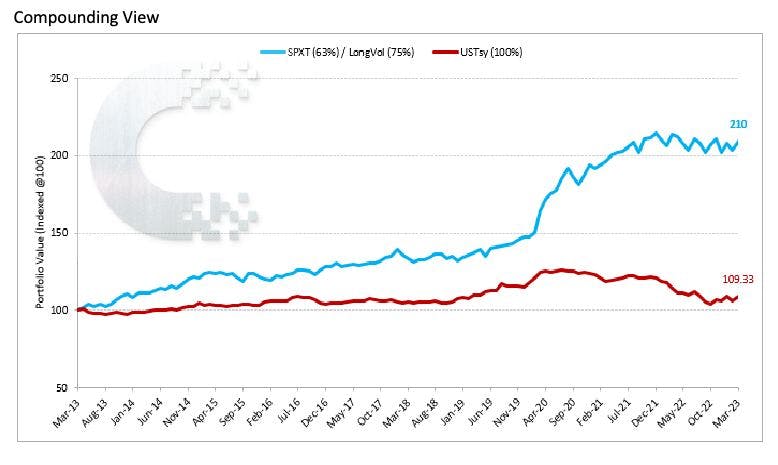

The red line in the above chart represents the performance of the standard, most commonly recommended 60 / 40 portfolio – wherein 60% is invested in equities, and the other 40% is allocated to bonds via an investment in the Bloomberg US Total Return Index. The blue line is a portfolio that has maintained the standard 60% equity allocation, but taken the remaining 40% of its assets typically allocated to bonds and put 62.5% of it into equities and 2x leveraged the other 37.5% with LongVol proxies (so 75% exposure). As you can see, the blue portfolio that has zero allocation to bonds has outperformed the standard 60 / 40 portfolio by 100% over the last decade.

This raises an important question: why the fuck is your fund manager still holding long-term government bonds? The answer is that the entire fiat financial system is structured to force – or at the very least heavily suggest – that owning government bonds is the fiduciary duty of your pension fund manager. Failure to follow that prescription could result in the loss of their job, which is the absolute last thing any citizen of Sharpe World wants. It’s great to be a mediocre muppet in Sharpe World and make millions of dollars per year while you repeatedly fuck your clients, all while following the rules.

But at some point, once you have lost enough of your clients’ money, your clients demand a change in tactics. And that is what the central bankers are going to need to manage. In the face of persistent inflation, banking failures, and the strong performance of alternative hard assets like gold and Bitcoin (which maintain or increase their energy purchasing power over time), how do you convince investors to continue losing money by holding government bonds?

The reality is that there isn’t a persuasive argument in the world strong enough to keep investors married to such a losing bet. So instead, governments have to force investors’ hands – which they typically do by simply erecting barriers to stop capital from exiting the system. It’s a bit trickier than that for the US, though, because if it were to enact explicit capital controls that affected crypto or any other asset outside the system, the USD would cease to be the global reserve currency due to the closure of its capital account. However, it would appear that the US has realized that if you make it just painful and expensive enough to access crypto, then the majority of the mass affluent and below will simply not bother – with their short attention spans forcing them back to their IG and TikTok feeds. Thirst Traps or Thrift???

The US is very keen to prop up Sharpe World because it is the greatest beneficiary of Sharpe World’s existence. US universities are the indoctrination centers for denizens of Sharpe World. These folks fan out across the world to ensure that everyone adheres to a global financial system that continues to put the USD, long-term Treasury bonds, and the major money (JP Morgan, Goldman Sachs, Citibank etc.) on a pedestal. Given that America stopped making stuff decades ago and decided to export financial engineering instead, it makes sense for the US to continue ensuring everyone plays by the rules of Sharpe World. When there is a threat to that status quo, the entire system will close ranks and do what is necessary to ensure capital never leaves.

The US population makes up about 4% of the world’s population. That is an extremely small slice of the pie, but those 4% are quite wealthy relative to everyone else globally. That is why we as investors care about what such a small population does with their money.

However, this wealth isn’t evenly distributed across the American masses – it’s highly concentrated at the top. 70% of America’s wealth is held by just 10% of Americans.

The majority of America is flat broke, and thus irrelevant when it comes to global capital markets. You might retort that casinos make a lot of money from poor people. My response is that while the floor of a casino is full of desperate punters pining after an easy path to riches, the real money – and what drives quarterly revenue – is made upstairs in the private rooms by the whales. You can’t build Vegas, Macau, Monaco etc. off the backs of people playing the nickel slot machine.

Put aside the wealthiest 10%, and let’s focus on the next rung down on the American economic ladder: the mass affluent. As I mentioned earlier, I define this term as encompassing all households that make $100,000 to $200,000 per year, which is roughly 25% of the nation.

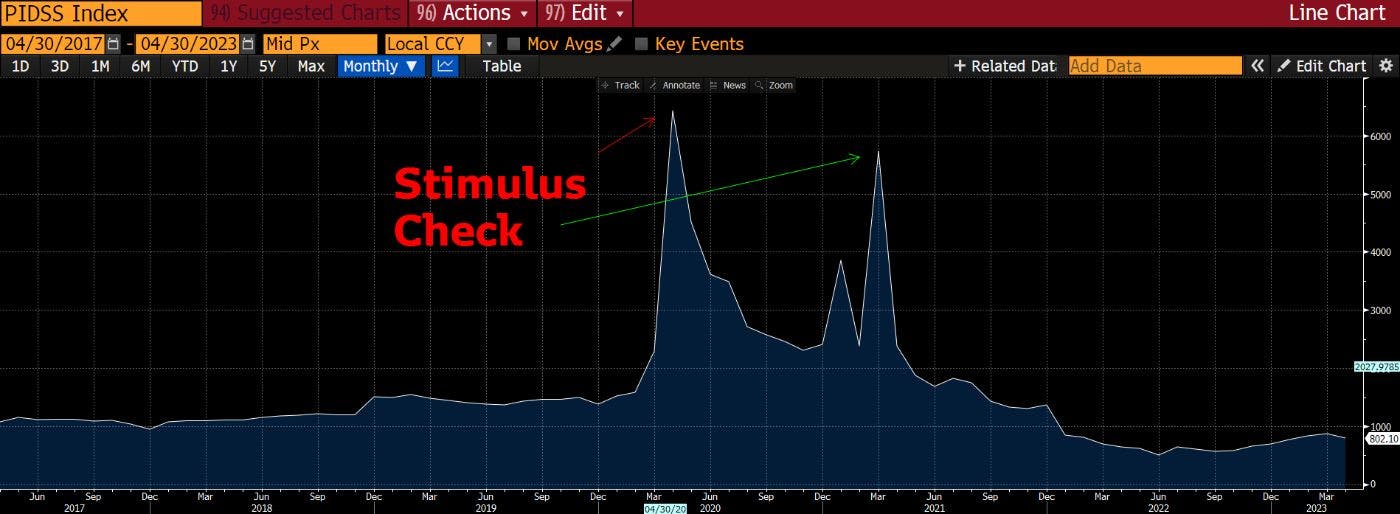

The important thing about this cohort is that, when COVID hit, they were most likely employed at a job that could be done from home. So that when lockdowns and stimulus checks came, they didn’t need to use that government handout to tide them over until they could go back to work. They basically had extra income to consume or invest in whatever they pleased.

This is the cohort that powered the surge in signups for online brokers like Robinhood. This is the cohort that got their first taste of degen crypto trading in 2020 and 2021.

The two spikes in US personal savings are due to the government stimulus checks. The bulk of the money was spent between 2020 and 2021, which is why you see the savings amount returning to the long term average. Errbody broke again!

This cohort drove the market higher during the COVID crypto boom. However, this cohort is not actually that wealthy. They might have a few quarters to rub together, but the financial intermediaries that make money catering to wealthy folks won’t open accounts for this cohort. The mass affluent fall squarely in the retail camp, and therefore have limited ways to easily access crypto. Coinbase, Kraken, Gemini, Crypto.com, Binance.us, and Robinhood are some of the major platforms that these retail investors are forced to turn to.

The reason why these exchanges and fintech players were so highly valued during the last bull market is that they catered to the mass affluent, which – courtesy of the USG – had a lot of disposable income to invest. However, without the services of these retail-focused fintechs, the mass affluent would be left without an easy means of accessing the global crypto markets.

Let’s conduct a little thought experiment. Assume that, due to the changes in the regulatory winds of the US, these fintechs must suddenly delist most of the tokens they trade, and/or cease offering crypto trading services entirely. (Crypto.com is an example of a company that recently exited the US market.) That would remove the American mass affluent from the equation entirely, eliminating a seemingly large pool of capital that would otherwise re-buy into the crypto markets when they felt wealthy again. That sounds really bad, but it is actually irrelevant.

The reason this cohort got involved in crypto in the first place is because of a government handout. But, the COVID stimulus checks proved to be so obviously and deeply inflationary that I don’t believe the monetary authorities will engage in such behavior again in the near future. Instead, the US Federal Reserve (Fed) and the US Treasury will return to handing free money to rich people via interest on government bonds and central bank deposit facilities (a process I described in detail in my last essay, “Patience is Beautiful”). That is how they usually juice financial markets.

If the government chooses to distribute another round of freshly printed money, but in the form of interest, rather than stimmy checks, it will not go to the mass affluent, who have little to no savings. The money will instead flow straight to the top 10%, and maybe even just the top 1%, who hold the majority of wealth in America. This wealth will then find its way into various forms of hard assets and stores of value. Due to their wealth, the 1% has a plethora of advisors pushing this or that solution to earn as much return on their money as possible. These are the most overbanked people in the world. Even though they are American, they have access to any and all financial assets traded globally – which means that if this rich cohort comes to believe that Bitcoin and crypto perform well in an inflationary environment, then they can easily buy it from a dealer who specializes in selling crypto to rich folks. I’m talking about firms like Cumberland, NYDig, and the OTC trading desks of the US-domiciled crypto exchanges like Coinbase and Kraken.

The point I’m trying to make is that, despite all of the hand-ringing going on in the crypto markets, it’s actually completely irrelevant whether the mass affluent and below can own or trade Bitcoin or a subset of shitcoins. They are broke, and the government ain’t handing out checks anymore. Even if Robinhood still allowed them to trade XYZ shitcoin, they wouldn’t have the available capital to purchase it anyway. The capital of the rich, on the other hand, is much more plentiful, and it’s fungible across the entire globe – all thanks to a host of intermediaries that cater to the American wealthy and will dutifully do whatever they are told as long as they receive a phat commission.

China and Japan hold the most amount of US Treasury bonds of any nation. That is because they both employ the same economic model:

This is the simple economic model of “Asia”. The competition between major Asian exporters at this stage is mainly on price, and price is dictated mostly by the value of each nation’s currency. As a result, the Chinese and Japanese care more about the CNYJPY cross than the cross of their currencies vs. the USD.

So who is the most price-competitive nation right now?

I indexed the USDCNY and USDJPY exchange rate at 100 from 1 January 2009 until 12 June 2023. As you can see, the JPY has weakened about 50% more than the CNY over the period – but perhaps most notable is the fact that the spread between the two has widened considerably since the onset of COVID.

Below I added CNYKRW (China vs. South Korea, white) and CNYEUR (China vs. essentially Germany, yellow) to round out the competitive landscape of global exporting powerhouses.

China is 3% cheaper than Korea, but 25% more expensive than Germany using this simple metric.

It makes total sense that the yen has depreciated so sharpley against the yuan because BOJ has continued to print more and more money in its attempt to hold Japanese Government Bond yields at certain levels. This is called Yield Curve Control (YCC). Post-COVID, China has not yet engaged in such a large degree of money printing or credit issuance to artificially pin bond yields to specific levels. Therefore, it is totally reasonable that the JPY has weakened against the CNY by 46% since 2009.

Chinese goods are expensive relative to Japanese goods. That has taken a toll on export volumes, and recent data confirms this.

The major bite of zero-COVID inspired lockdowns started in the summer of 2022 – we can see from the above chart that exports crashed right around then. Then, Beijing abandoned zero-COVID overnight and reopened. Exports surged again as people got back to work. This bust to boom trajectory obscured the general weakening of the global consumer and the waning price competitiveness of Chinese goods.

This chart tells a similar story to that of exports.

China is now fully open, and there should be no lingering effects of the 2022 lockdowns. However, exports are now falling on a YoY basis. Not good. And while all of this was happening, JPY weakened massively against CNY. If the global pie is shrinking, China needs to become more competitive vs. its major export competitors in order to maintain the growth necessary to placate its populace.. Its number one competitor is Japan (and remember, they have identical economic models). The yuan MUST weaken vs. the yen to help boost Chinese growth.

The biggest reason the Chinese Communist Party (CCP, or “The Party”) needs growth is that they have a massive unemployment problem. Specifically, urban youth unemployment is over 20%. There are just not enough jobs for high school and university graduates.

For those of you who don’t know, graduating university in China is a big deal because it is so difficult to get in. High school students take what is called the GaoKao (the literal translation is “a big test”). If you don’t score high enough, you do not get into university. There ain’t no rocks for jocks in China. Therefore, children and parents are completely focused on this test from the moment primary school begins. In a country so big, how do you evaluate who to hire or not? You fall back on things like test scores and university attendance to an even larger degree than in the West.

For the past 40 years, parents who spent all their energy and money to coach their one little emperor through the schooling system have been rewarded. University graduates got jobs that paid better than manual repetitive factory work, moved to a city, and got HuKou (residency). Success!

But now, after possibly destroying the vibrancy and fun of childhood by studying all sorts of nonsense that Tiangong (the Chinese version of ChatGPT) can regurgitate with perfect accuracy back to you in a millisecond, you graduate from university and get no job. China has a vast underclass of extremely educated and jaded young people. This is the literal worst nightmare of a Marxist who believes the intellectual bourgeoise can foment the seeds of revolution if left unchecked. Xi Jinping is a student of Mao and certainly realizes his Party must generate jobs to get the youth back to work.

When in doubt, China resorts to policies that support exports and infrastructure projects to boost growth and employment. The supply-side economic measures that got China to where it is today are likely to be repeated, even if it means piling on more unproductive debt atop an already gargantuan heap. This requires a weaker yuan.

To weaken the currency, the PBOC will encourage credit growth in the “good” sectors of the economy. Semiconductors, AI, clean energy, property etc. will all have higher loan quotes. The banks will be instructed to lend a certain amount of yuan to these sectors, or else. It won’t matter whether these businesses actually need the capital.

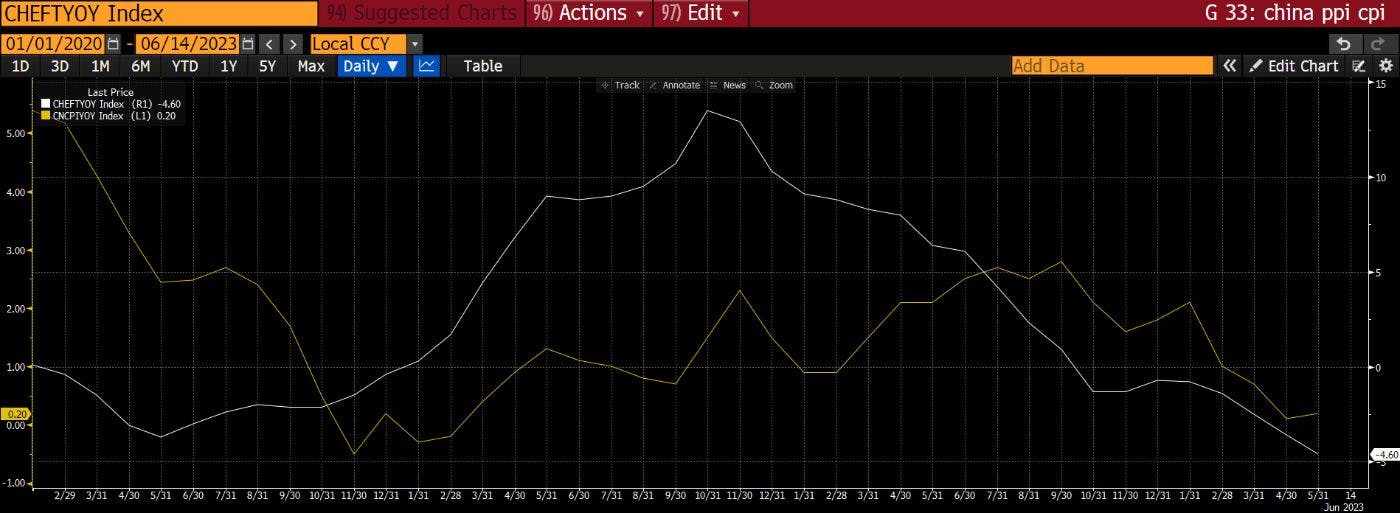

As credit expands, the currency will be allowed to weaken. The PBOC might do a one-off shock devaluation and then guide the CNY slowly downward, weakening it over time against the JPY.

With both PPI and CPI in negative territory, the PBOC can ease without fear of stoking inflation.

Because some of this capital isn’t needed by high-quality firms, it will “leak” into financial assets (much like the American mass affluent stimmy checks did). There are various ways in which companies that should be making widgets will end up getting loans and use them to speculate in the financial asset markets. And most importantly to this essay, the Chinese mass affluent – who see what is coming – will start to spirit capital out of China.

In the past, the PBOC might be worried about capital flight, but the hoard of Western fiat financial assets “owned” by China has become a liability, rather than an asset. That is because the West has turned from friend to foe. Who knows what will happen in the political circles of the West vis-a-vis Chinese capital. It is entirely possible that we all wake up one day and a select portion of China’s assets have been frozen because of some action that displeased the Western political elites.

Regardless of whether you are a democratically elected president, a dictator, or an emperor, politics is all about cover your ass (CYA). How does the Party CYA with respect to China’s state-owned foreign assets? It allows the wealthy to exchange CNY for USD and buy stuff. Then, if the wealthy Zhou gets his NYC brownstone yanked because he is a rich non-white foreigner, that’s his problem, not the Party’s.

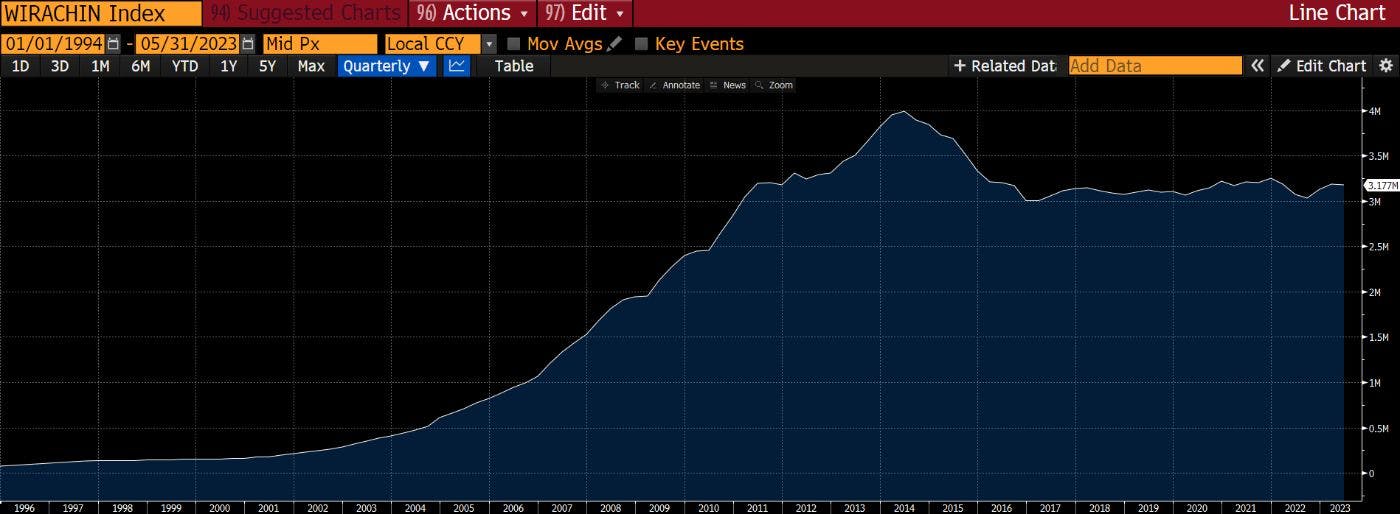

As you can see, China has a roughly $3 trillion dollar “problem”.

The even better policy would be to allow the wealthy to purchase hard assets like crypto, and ensure they are stored in China by fiduciaries they own or control. I have predicted before and continue to believe that Hong Kong will be the conduit through which Chinese capital is allowed to own crypto financial assets. When I say financial assets, I mean ownership of the financial returns of the underlying crypto tokens or currencies, likely through funds or derivatives – because Beijing is not interested in letting its constituents actually hold technology that allows for real, non-state backed economic freedom. In this way, Chinese investors sell down the fiat dog shit on the state’s balance sheet and replace it with Bitcoin and other cryptos. Viewed as one common whole, the Chinese nation would have a stronger balance sheet after such an action.

This is how I imagine the flow could work:

This solves many problems for China:

For us crypto HODLers, this is a great outcome. The return of the Chinese crypto trader through the financial pipes of Hong Kong will reignite the market at the same time the broke-ass American mass affluent are effectively shut out. The beauty of this is that each nation state’s action drives the other nation state to do more of the same.

The mere act of China weakening its currency and allowing loyal comrades to buy Bitcoin derivatives in response reduces the amount of Western fiat assets the country holds. The more reluctant China is to purchase US Treasuries with its export earnings or to hold USD assets in any form, the harder the US must work to ensure its citizens’ capital can’t leave Sharpe World since the usual buyer of long-term debt, China, is on strike. It’s a positively reflexive relationship that should deliver glorious returns to Lord Satoshi’s faithful.

This article was originally published by Arthur Hayes on Hackernoon.

World Economic Forum (WEF) founder Klaus Schwab tells Swiss media he's exploring ways to choose…

Adults today spend over nine hours a day sitting, according to national health data. On…

The web has a WordPress problem – not the platform itself, but the people who…

Neural rights was a hot topic during a session called "Approaching Singularity: Our Brains Interfacing…

At some point in the last 10 years, I started viewing Colonel John Boyd as…

When I started designing an AI Evaluation pipeline/framework at my organization, I had no idea…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}