The credit card rewards system operates on a structural imbalance that rarely gets discussed openly; every time a consumer redeems miles for a flight upgrade or points for a hotel stay, the financing behind those benefits has often come, in part, from people who can least afford it.

Economists estimate that more than $15 billion USD flows annually from lower-income to wealthier Americans through the credit card rewards system. The mechanism runs through interchange fees: merchants pay a cost on every card transaction and, bound by contract from passing that cost to high-rewards cardholders specifically, absorb it into prices paid by all customers.

The result, as analysts at the Brookings Institution have noted, is that lower-income consumers and merchants effectively subsidize the rewards accruing to wealthier ones.

The broad debt picture compounds the problem: Americans’ total credit card balance reached $1.277 trillion in the fourth quarter of 2025 – the highest figure recorded since the Federal Reserve Bank of New York began tracking in 1999 – and 61% carrying card debt have now held it for at least a year, up from 53% in late 2024.

Against this backdrop, New York-based fintech Debbie was founded. Co-founders Frida Leibowitz and Rachel Lauren both grew up in immigrant households, navigating debt and limited pathways to generational wealth.

The duo met as college roommates and built the startup’s first iteration while working to address Leibowitz’s own $15,000 USD in credit card debt. The experience shaped a clear thesis: the incentive structure of consumer finance needed to be reversed – not optimized.

Today, the company launched Rewards 2.0 and announced a $5.3 million USD seed round led by Trustage Ventures and Reseda Group, with participation from One Way Ventures and Zeal Capital Partners. Total funding now stands at around $8 million USD.

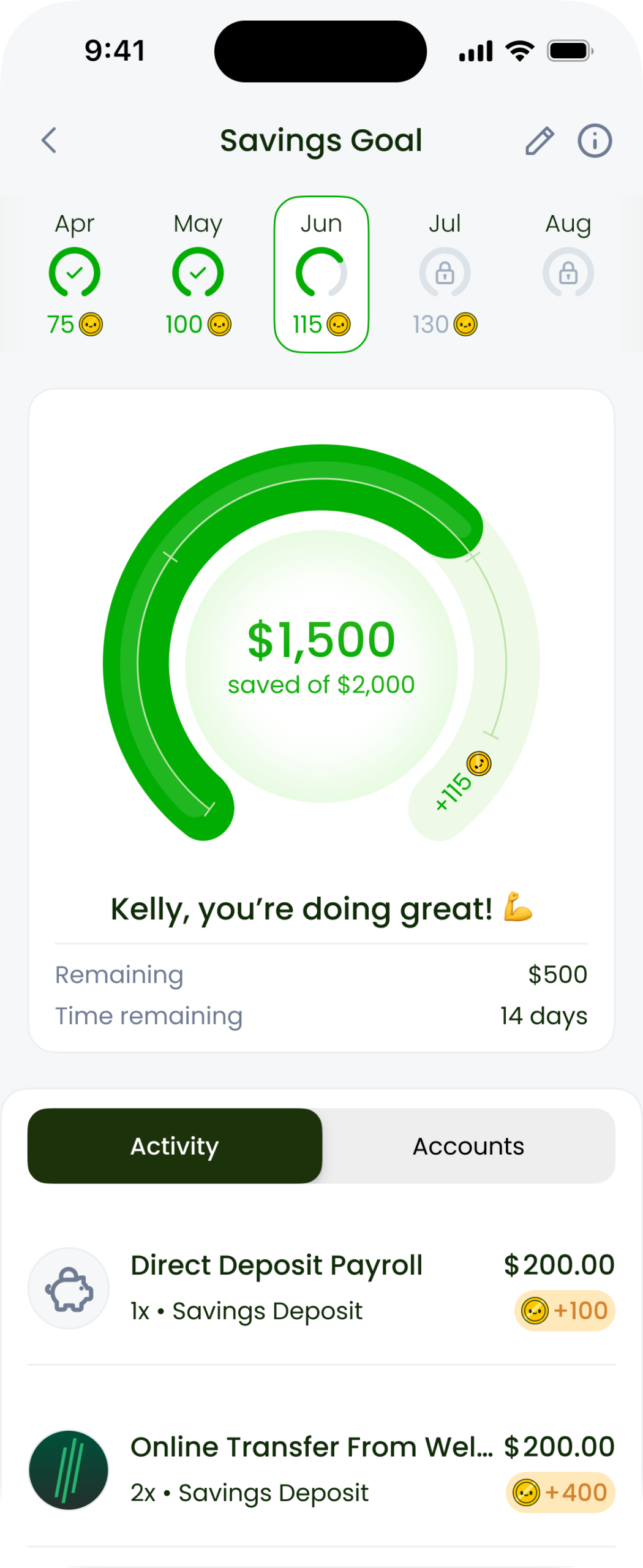

The rewards is a direct structural inversion of the traditional credit card points system; users earn one Debbie point per dollar deposited into savings or applied toward paying down a credit card balance – points redeemable directly for cash.

Beyond this, accounts held with eligible partner banks and credit unions unlock 1.5x to 2x point multipliers. Additional points are available for completing in-app financial education modules and maintaining monthly saving streaks.

Debbie currently operates with 11 bank and credit union partnerships, with the alignment designed to be mutual: financially healthier users translate into greater deposits, giving institutions a commercial rationale for participation.

The platform has reached over 200,000 users, who have collectively earned more than $2.3 million USD in cash rewards and saved $149 million USD toward stated financial goals – figures the company presents as evidence of genuine behavioral change rather than passive engagement.

“The problem isn’t that Americans lack financial tools – it’s that the incentive system is backwards,” said Leibowitz.

“Loyalty programs overwhelmingly reward spending, even though most consumers should really focus on paying down debt and building savings. We’re flipping that incentive model to reward financial progress instead.”

The launch arrives at a notable time in the credit card market: last year, major issuers including American Express and Chase overhauled their flagship premium products, raising annual fees and deepening perks oriented toward high-spending cardholders – accelerating bifurcation between customers the legacy system serves well and those it doesn’t.

The average personal savings rate in 2025, in fact, stood at just 4.6% of disposable income, representing less than half the rate sustained through the 1960s and 70s.

Lex Zhao, general partner at One Way Ventures, described the proposition in straightforward terms: “Debbie uses real cash to incentivize users to build savings and reduce debt. It’s an incentive that directly mirrors the appeal of traditional credit card points, but that actually supports healthy financial behavior.”

Planned expansions to the rewards ecosystem include gift card redemptions, exclusive events, and points transfers to major merchants – broadening the platform’s utility for a consumer segment that the existing loyalty landscape has largely left underserved.

Featured image: Ruliff Andrean via Unsplash+

Disclosure: This article mentions clients of an Espacio portfolio company.